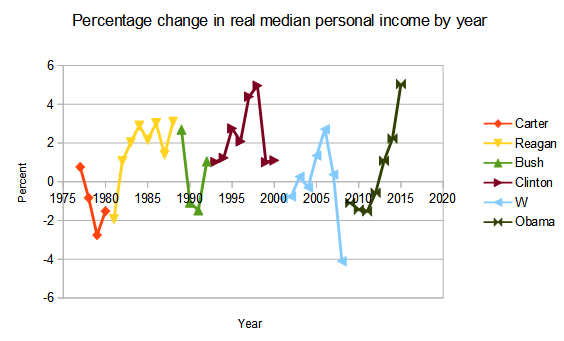

The winner here is Bill Clinton, with Ronald Reagan a strong second. This chart clearly shows that some Presidential terms are much better for workers than others. Obama's performance was very poor in his first term, and he is going to finish well behind Reagan and Clinton.

Below I show the same data displayed in a different way. Real income growth in 2015 was the strongest in the past 40 years. Another few years of that kind of performance would be very helpful for American society.

How do modern Presidents compare with those from the 1950s and 60s like Eisenhower, Kennedy and Johnson? The real median personal income data only goes back to 1976, so I went looking for another income data series. The best I found was real compensation per hour for the non-farm business sector. The deterioration in performance from the era of Eisenhower to modern times is really quite shocking. There is a big step down in growth after 1970 and another one after 2008.

This measure shows that President Obama has had the worst growth in real hourly compensation of any President since at least 1953. Real hourly compensation data looks worse for Obama than real median personal income. Hourly compensation is linked to wages, while personal income includes investment income and other income sources as well as wages.

Notes and data sources

1/ All data is from FRED. I am using the non-seasonally adjusted Real Median Personal Income in the United States series set to show percent change from a year ago. I get non-farm real hourly compensation from here.

2/ 'W' is George W Bush who was President from 2001 to 2008. 'Bush1' is the first President Bush who served from 1989 to 1992.

3/ Carter served from 1977 to 1980. Reagan served from 1981 to 1988.

4/ 'Real' income shows growth in purchasing power after inflation is taken into account. 'Median' income is more relevant to the middle class than average income, which is increased by rising incomes among high earners.